PropNex Picks

|April 22,2025Can You Retire Off Your First and Only Property?

Share this article:

In Singapore, it's no secret that real estate can give you the golden ticket to a comfortable retirement. After all, property appreciation here is relatively steady and rental income is a nice bonus. But is it possible to retire from your first and only property? Let's break it down!

Did you know that Singapore is the most expensive city in the world according to EIU's Worldwide Cost of Living survey? And that we have maintained this position for the ninth time in the last eleven years? This means you need to reserve a substantial amount for your retirement savings.

A 2019 study involving 100 participants found that elderly singles need $1,379 per month to meet basic needs, while elderly couples need $2,351. For single persons aged 55-64, it's at $1,721. That number would be even higher if you're aiming for a more comfortable lifestyle. Think travel, dining out, healthcare, and entertainment.

If you consider inflation and rising costs of living, these estimates are actually already outdated. Today, the required amount is likely much higher, and by the time you decide to retire, it will only continue to increase.

Ideally, you'd live longer and retire earlier, but for the sake of example, let's assume you live until 85 and retire at 65. That's 20 years of living expenses. You'd need $330,960 to cover the bare minimum if you retired six years ago. If you want to retire comfortably years down the line, also accounting for inflation and other costs, you'd need way more than that, perhaps in the seven figures.

Let's say you try to stretch your first and only property into a retirement plan. You're probably getting a BTO since that's the most affordable option. Then, you stay there for life, hoping for the best.

Living from paycheck to paycheck

Eventually, you might live mortgage-free. But you'd still have to depend on your salary and CPF to survive even though you're technically sitting on hundreds of thousands in potential profit. Unfortunately, it won't mean anything unless you sell. If you do, where will you live then?

To make matters worse, bank interest rates are miserable, so your savings won't grow fast enough to keep up with the times. Meanwhile, inflation keeps going up. Food, transport, healthcare, everything becomes more expensive every year.

Slowly drowning from inflation

It surely doesn't help that wage growth is losing to inflation rates. Over the years, we know that wage growth slows down. Meanwhile, the Consumer Price Index (CPI) inflation rate, which tracks the cost of things like food, transport, and housing, continues to rise. By 2021, the lines intercept, showing the point where inflation overtakes wage growth.

Side hustle?

Sure, you can rent out a spare room to make ends meet, but the amount you get from partial rent is not going to make that big of a difference. Plus, you'll have to share your home with a tenant... for life. Is that really the kind of retirement you've been dreaming about?

Alternatively, you can consider HDB's Lease Buyback Scheme (LBS). Under this scheme, you can sell part of your flat's remaining lease back to HDB and receive a cash payout while continuing to live in your home. But, you have to leave enough lease to cover you until the age of 95. So if you're 65 years old, you need to retain at least 30 years of lease. This scheme is designed to help seniors unlock value from their flats without moving out.

So, how much can you get from this? The majority of households that have opted for this scheme received $100,000 - $300,000. Is that amount really enough to last you 30 years? Besides, resale HDB flats nowadays can go for much more than that. Some even sold for more than $1 million! So yeah, I personally wouldn't recommend the LBS. You're giving up future value for present-day survival. Once that money runs out, that's it. No resale value left, no fallback. It's more of a last resort than a real plan.

And even if you don't sell your remaining lease, your property will eventually get eaten by lease decay. This means your property's value declines as the lease runs down, making it harder to sell. Since everyone also wants to avoid lease decay, you'll attract fewer buyers, especially as your property nears its 40th year. Plus, there are financing limitations for older properties.

Passing on the responsibilities

Regardless, who do you think is going to deal with all that after you're gone? Your children. Instead of leaving them with assets that could help their future, you're passing down a property that might not be worth anything. I'm just saying, your decisions don't just shape your future, but your childrens' too. Wouldn't you want something better for them?

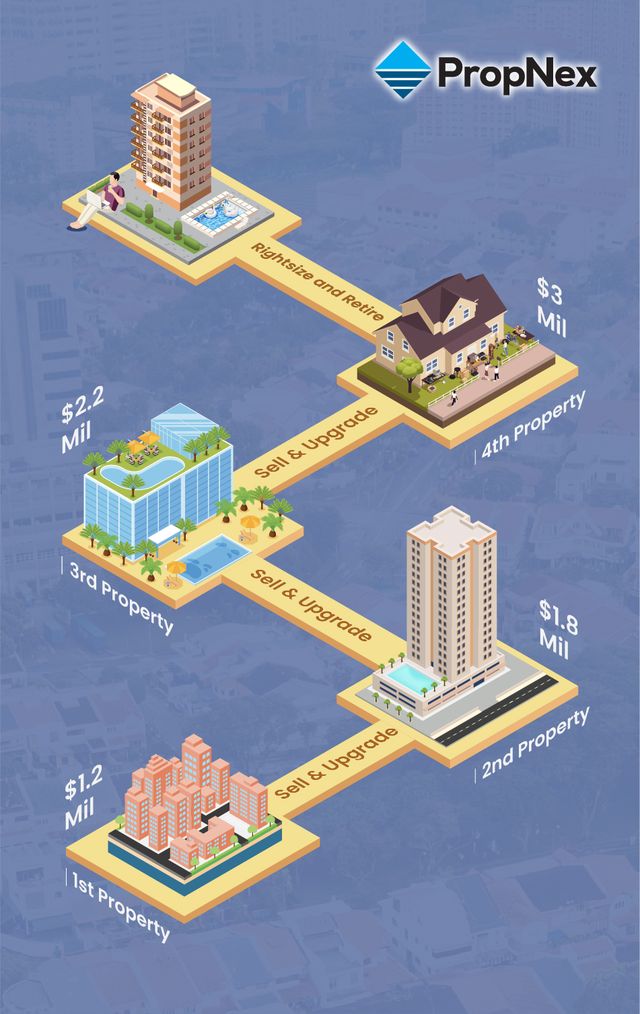

Well, it starts with... buying a property! It doesn't matter if you start small, you just have to start. Once the property appreciates, sell it for a profit to build wealth and lay the foundation for a solid investment portfolio.

From there, you can keep upgrading to a bigger or better-located home while you're still earning, accumulating wealth with each move. Then, when you're ready to retire, you can right-size. Sell your highest-value property and move into a smaller but comfortable home. This way, you free up cash for your golden years.

Imagine if you start doing this at age 30, upgrading every five to ten years. You could build enough wealth to retire comfortably by 65, or maybe even sooner!

Basically, the key here is leveraging capital appreciation, which has historically been steady in Singapore. In fact, over the past 20 years, private residential property prices have increased by 157.6% and HDB resale prices have risen by 156.7%. So take advantage of the resilient and stable housing market that is right in front of you!

Once you've accumulated enough assets and perhaps have enough to own more than one property, you can then start thinking about earning rental income. As of Q4 2024, the average rental yield in Singapore was 3.40%, which doesn't seem like much if you're relying on just one home. That's why you should invest in multiple properties, so that your passive income from rent can comfortably cover your expenses, add to your retirement fund, and speed up the process a bit.

Unless you're earning like, $50,000 a month, the answer is no. For the average Singaporean, retiring off just one property is nothing but a fantasy. Your retirement plan should ensure long-term financial security, and that means one property for a lifetime is just not enough.

The only sustainable way to retire comfortably is to leverage your property for growth (not just sit on it!). Retirement isn't about luck. It's about strategy.

So the real question is: Are you ready to start building that strategy today?

If you're serious about taking the next step, join us at our upcoming Property Wealth System (PWS) Masterclass to hear experts break down proven property strategies, show you how they have done it, and help you plan the retirement you deserve.